Subtotal $0.00

Email : 35

BenefitMargin subsidy: General 15% (urban), 25% (rural); SC/ST/Women 25% (urban), 35% (rural)

Valid Till31 Dec, 2030

Scheme CodePMEGP

PMEGP Scheme 2026: Startup Loan and Subsidy Guide

The Prime Minister’s Employment Generation Programme (PMEGP) is a central-government initiative (launched in 2008) that funds new micro-enterprises to create jobs. Administered by the Ministry of MSME and implemented nationwide by the Khadi & Village Industries Commission (KVIC), it provides credit-linked bank loans with a government subsidy. In practice, the government pays a portion of the project cost (15–35%) as margin money, and you repay the rest as a normal loan. Note that PMEGP is not a free grant – founders must contribute their share and repay the loan, so preparing a solid business plan is crucial.

What is this scheme?

PMEGP is essentially a credit-linked subsidy scheme that merged two older programs (PMRY and REGP) into one. Its goal is to generate continuous employment in both rural and urban areas by helping entrepreneurs set up micro-enterprises. As a national-level scheme, it has no income ceiling and is implemented through KVIC (at national level) and State Khadi boards/DICs. In simple terms, PMEGP lets eligible first-time entrepreneurs access bank loans at regular interest rates, but with a significant portion of the project cost covered by a government subsidy. (The ultimate loan approval is still done by the bank’s credit committee.)

Who is this scheme for?

Anyone over 18 with a new business idea can apply. Individuals (with at least 8th-grade education if project >₹10L manufacturing/₹5L service) are eligible. Self-Help Groups, cooperatives, registered societies, and charitable trusts can also apply. There is no income test, so both low-income and higher-income founders are covered. Critically, only brand-new enterprises qualify – existing businesses or ones that have already received government subsidies are not eligible. In practice, PMEGP targets first-time entrepreneurs (urban or rural) who want to set up small manufacturing or service units. (For example, someone planning a new food-processing unit, a small factory, a repair workshop, etc., could apply.)

What support does it offer?

PMEGP provides two main supports: a bank loan and a government subsidy. The subsidy (called margin money) is paid by the government directly to your account and reduces the total project cost. Subsidy rates range from 15% (urban general category) up to 35% (rural special category) of your total cost. The rest of the funds come as a term loan from a scheduled bank. For example, in a rural special-category case (say a woman entrepreneur or SC/ST), the scheme might cover 35% of costs, and you would invest about 5%, while the bank loans the remaining 60%. Entrepreneurs typically contribute around 5–10% of the project cost (10% for general category, 5% for special), and the bank lends the balance (90–95%).

The loans are offered by many banks (27 public-sector banks plus some regional/co-operative banks and selected private banks). An added benefit is that loans up to ₹10 lakh do not require collateral. (For larger loans, the government provides a CGTMSE guarantee up to ₹25 lakh to ease bank risk.) In short, PMEGP is a subsidized bank loan scheme: you repay only the loan portion, while the government chip in a substantial subsidy on top.

Key benefits founders should know

- Subsidy lowers your cost: The government covers a significant percentage of your project, so you borrow less.

- Flexible eligibility: No income ceiling and open to many (individuals, SHGs, co-ops, trusts) means even low-income or rural entrepreneurs can apply.

- Higher subsidy for special categories: If you’re a woman, SC/ST, minority, ex-serviceman, or in a hill/NE area, you get the top subsidy rates (25–35%).

- No collateral for small loans: Loans up to ₹10 lakh are secured without collateral, and the rest up to ₹25 lakh carry a government guarantee.

- Skill support: Mandatory entrepreneurship (EDP) training (for larger projects) improves your business planning.

- Widespread availability: The scheme is nationwide (all-India). Over two dozen banks participate, so applicants can often find a nearby branch to work with.

When this scheme makes sense

PMEGP is ideal when you want to start a brand-new micro-enterprise and need structured financing. It fits entrepreneurs who have a clear business plan and need funding within the scheme limits (project cost up to ₹25 lakh for manufacturing or ₹10 lakh for a service unit). Specially:

- If you are a first-time entrepreneur (with or without prior job experience) and want to set up a small factory, workshop, service outlet or trading venture, this is a good option.

- If you fall into a special category (woman, SC/ST, etc.) or operate in a rural area, PMEGP is especially appealing because you receive a higher subsidy.

- If you are willing to develop a detailed project report and attend entrepreneurship training, you’ll meet the scheme’s expectations (banks look for a solid plan).

- If you prefer a formal loan with government backing over seeking grants or private equity, PMEGP can make bank financing more accessible.

In summary, PMEGP makes sense for early-stage startups and microenterprises that need moderate funding and are ready to navigate the bank loan process (with government support).

When this scheme may not be suitable

- Not for expansions or old businesses: If you already run an existing enterprise, PMEGP won’t help – only new units are covered.

- Too large a project: If your required funding exceeds the scheme cap (over ₹25 lakh for manufacturing or ₹10 lakh for service), you’ll need a different source.

- Looking for grants: PMEGP is not a grant. It’s a loan (with subsidy). If you can’t or don’t want to repay a loan, look elsewhere.

- Disallowed activities: Certain small retail or agricultural projects are excluded (check the scheme’s negative list). For example, basic grocery shops or farming units like poultry/goatery generally don’t qualify.

- Urgency & preparation: If you need funds immediately or can’t invest time in preparing a project report and training, PMEGP may be frustrating. Bank approvals typically take weeks to months, so this is not a quick cash scheme.

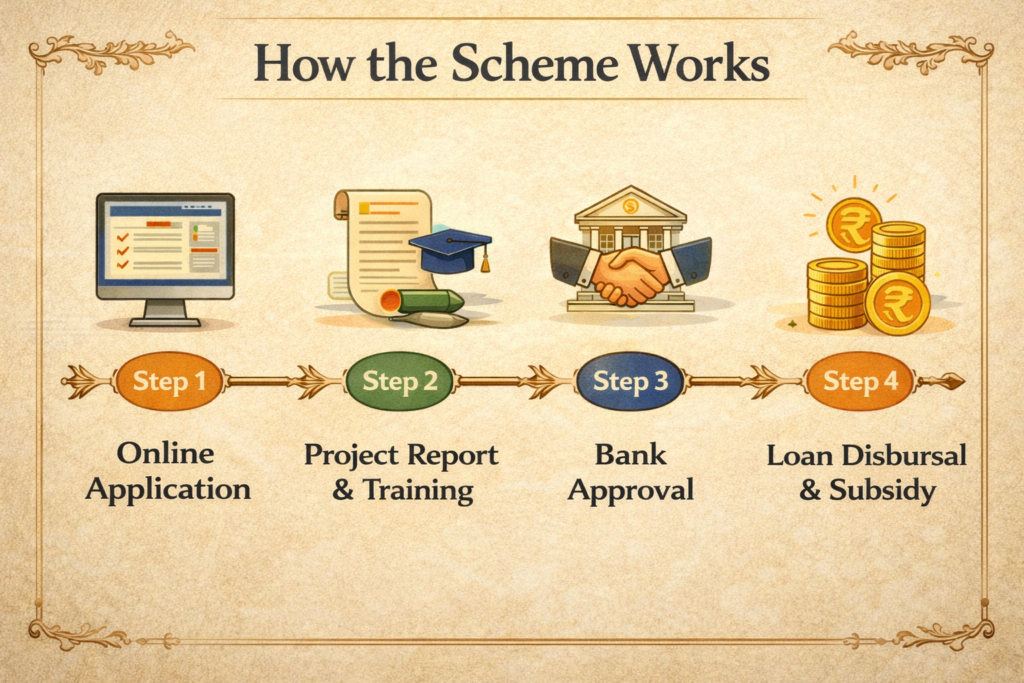

How the application process usually works

Applying to PMEGP has two main steps: online submission and bank approval. First, you create an account and submit your project on the KVIC PMEGP portal. Fill in details, upload your project report and documents (ID proof, address, certificates, project cost estimates, etc.). (Model project profiles are available on KVIC’s site to help you craft your report.)

For projects above ₹5 lakh, you must complete a government-approved Entrepreneurship Development Programme (EDP) training (6–10 days) before claiming subsidy.

Once you submit online, your application goes to the local KVIC/KVIB/DIC office and then to the nodal bank for the district. The bank will review your project, often interview you, and do a credit appraisal. If the bank sanctions the loan, they disburse the funds for your capital and working capital needs. The government subsidy (margin money) is usually credited later, after you fulfill minimum utilization conditions and a 3-year lock-in period.

Overall, expect several weeks or more for approval. Persistence helps – follow up with the bank branch. Remember: portal submission is only the first step; final approval comes from the bank’s credit process.

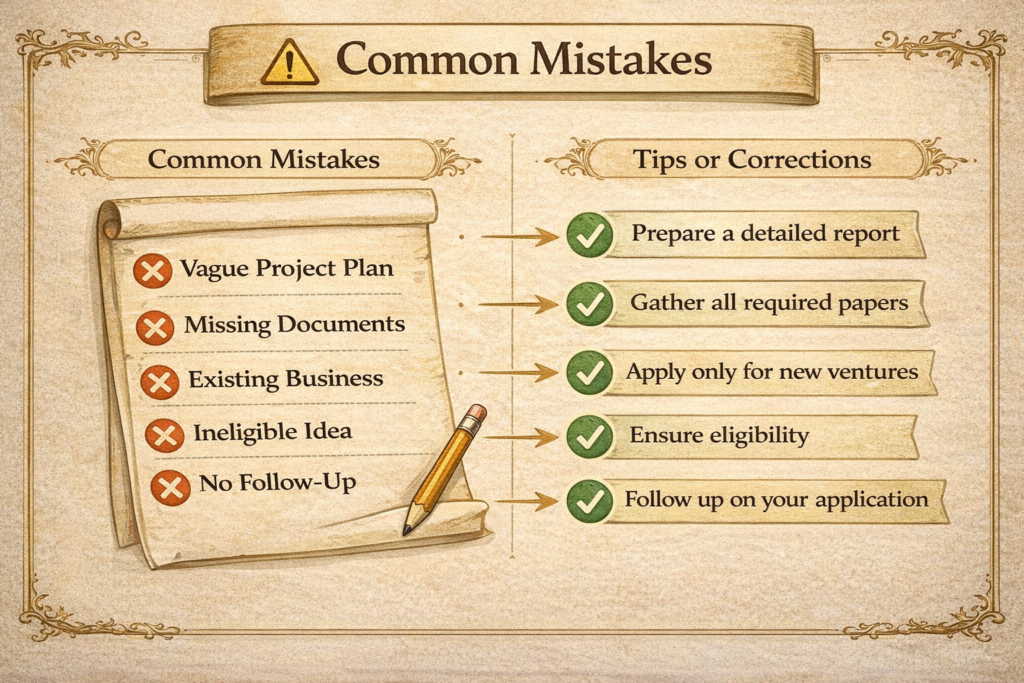

Common mistakes founders make

- Weak or incomplete project report: Banks want detailed, realistic plans. A vague plan or incorrect cost estimates often leads to rejection.

- Missing documents: Forgetting key paperwork (ID, PAN, education/caste certificates, project report, etc.) delays approval.

- Ineligible business idea: Proposing a venture outside PMEGP’s approved list (e.g. certain farming or retail activities) risks rejection.

- Applying for existing business: Using PMEGP for an already-running unit (even if small) is not allowed.

- Treating it like a grant: Expecting automatic funding or rushing the process is dangerous. PMEGP is a loan scheme, so you need follow-through and repayment discipline.

- Wrong bank branch: Some branches have more PMEGP experience. Not seeking guidance from the local KVIC/DIC office or picking a branch unfamiliar with the scheme can cause hiccups.

- Skipping training: If you don’t complete the required EDP, your subsidy claim can be held up.

- Poor follow-up: Assuming the portal alone secures the loan is a mistake. Regularly check status and stay in touch with bank officials.

Official source & verification

For authoritative information, refer to government/official sites and documents:

- KVIC PMEGP Scheme Page (Government of India): Details on PMEGP objectives and features.

- PMEGP Scheme Guidelines (KVIC PDF): Comprehensive rules on eligibility, funding norms, subsidy rates, etc..

- KVIC PMEGP FAQ Section: Common questions answered (subsidy %, max costs, eligibility, etc.).

- Ministry of MSME / Jansamarth: National portals listing PMEGP and related schemes (for application links and scheme notices).

These official resources confirm the details provided above and should be consulted for any updates or clarifications.

FAQs (Founder FAQs about PMEGP)

- Q: Do I have to be a woman or SC/ST to apply? No – PMEGP is open to any eligible founder (individual or group). Special categories (women, SC/ST, etc.) simply get higher subsidies, but general-category applicants are also accepted (with a lower subsidy rate). There is no income cap, so all entrepreneurs can qualify.

- Q: My small shop is already running. Can I get PMEGP for it? No. PMEGP only funds new ventures. If your business is already in operation, or if it has already received a government grant/loan, it is not eligible. You must set up a brand-new unit to use this scheme.

- Q: What’s the maximum funding I can get? Project cost limits are ₹25 lakh for manufacturing units and ₹10 lakh for service/business units. The subsidy portion varies: in urban areas general-category projects get 15% and rural 25%; special-category get 25% (urban) and 35% (rural) of project cost. You’ll provide 5–10% of the cost yourself and borrow the rest.

- Q: Do I have to repay the money? Yes. PMEGP is a loan scheme, not a free grant. You must repay the bank loan according to schedule. The government only pays a subsidy into your account (margin money) to reduce your loan burden. Treat it like any other business loan.

- Q: How do I apply, and do I need training? Apply online via the official PMEGP portal on the KVIC website. Fill the form, upload your project report and documents. If your project cost exceeds ₹5 lakh, you must complete a short entrepreneurship (EDP) training before claiming subsidy. After online submission, the local PMEGP office and the chosen bank will process your application.

- Q: Is collateral or guarantee needed? For projects up to ₹10 lakh, no collateral is required. Loans above ₹10 lakh may require security or the national credit guarantee cover (CGTMSE provides guarantee up to ₹25 lakh under PMEGP)

Read More Blog–Smart AI Workflows Every Startup Should Implement

Eligibility Criteria

Individuals (18+), SHGs, Trusts, Cooperative societies (new projects only)

🚀 Ready to Scale Up?

Don't miss this opportunity! Visit the official portal to check your eligibility and apply today.

Apply Now on Official Website →

Comments are closed