Subtotal $0.00

Email : 7

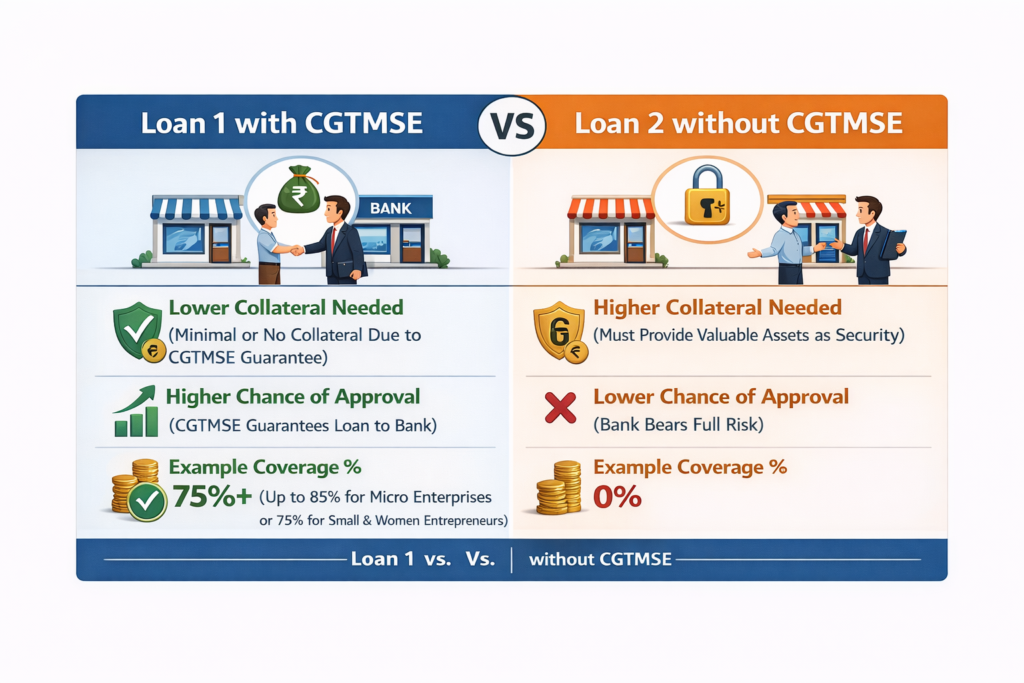

BenefitCollateral-free loans up to ₹10 crore; guarantee coverage: 85% (micro/women/NE), 75% (other MSEs), 50% (₹1-5 crore)

Valid Till31 Dec, 2030

Scheme CodeCGS 2000

CGTMSE Scheme 2023: A Startup Founder’s Guide

The Credit Guarantee Fund Trust for Micro & Small Enterprises (CGTMSE) is a government-backed loan scheme that helps small businesses and startups get bank credit more easily. For founders, this matters because banks often hesitate to lend to new ventures without collateral. CGTMSE provides a guarantee to the bank (covering up to 75–90% of the loan) so that your business can secure funds (for working capital or expansion) without tying up property or other assets. Recent Budget changes (effective April 2023) infused ₹9,000 crore into the CGTMSE corpus, enabling ₹2 lakh crore of additional credit and reducing the cost of loans by about 1%. In other words, more collateral-free credit is now available at a lower cost for MSMEs, making it easier for founders to raise funds (though note no scheme can guarantee a loan – the bank’s discretion and your business viability still decide).

What is this scheme?

CGTMSE is a credit guarantee scheme launched by the Government of India (Ministry of MSME and SIDBI) in 2000 to encourage banks to lend to micro and small enterprises (MSEs). Under CGTMSE, when a bank gives a loan to an eligible small business, the CGTMSE trust guarantees a large part of that loan. This means if the borrower defaults, the trust will pay the bank back up to a certain percentage (usually 75%, or more for special categories). In practice, this lets founders get bank loans without having to pledge collateral or third-party guarantees. A new “Hybrid” collateral model (introduced recently) even allows partial security: the bank can take collateral on part of the loan, and CGTMSE will guarantee the rest. Thus, CGTMSE facilitates easier access to credit for startups and small businesses by sharing the risk with banks.

Who is this scheme for?

CGTMSE is meant for Micro and Small Enterprises (MSEs) in India – essentially small businesses in manufacturing or services. Eligible entities include proprietorships, partnerships, LLPs, private companies and the like. The scheme specifically excludes agricultural ventures, Self-Help Groups (SHGs), and Joint Liability Groups (JLGs). In simple terms: if your business is registered as an MSME (with Udyam Registration) and operates a small manufacturing or service activity, you can apply. For example, a small bakery, a software startup, a roadside food stall chain, or a local manufacturer of goods would qualify. Importantly, even new enterprises (startups) count as eligible if they fall under these MSME definitions and have Udyam registration. Trading businesses (shops, retail) are now also covered on equal terms. Women-led, SC/ST-owned, or ZED-certified businesses get extra benefits (higher coverage, fee discounts) under the scheme.

What support does it offer?

Under CGTMSE, a bank loan to your eligible MSME can get a guarantee cover of:

- Up to ₹10 crore per borrower (latest ceiling). This is the total loan exposure that can be guaranteed.

- Loan coverage percentage: Typically 75% of the loan is guaranteed. Special categories get higher cover: up to 85% for SC/ST, PwD, etc., and 90% for women entrepreneurs or Agniveer beneficiaries. An additional 5% coverage is added if your business is in a government-identified “credit deficient” district.

- Collateral requirement: Normally no collateral or personal guarantee is required for the guaranteed portion. In the hybrid model, the bank may take collateral for part of the loan, and CGTMSE will cover the unsecured portion (up to ₹10 cr).

The founder’s practical benefit is that banks lower their lending risk. In effect, your business could qualify for a working capital loan or term loan without having to mortgage property. For banks, CGTMSE acts like a partial insurance: if the loan goes bad, the trust pays the guaranteed amount (subject to scheme rules). This means startups can invest in equipment or scale up operations with less collateral. Also, the guarantee cover applies to standard credit products (term loans, working capital, even retail trade loans).

CGTMSE does have a small fee: the bank typically charges an annual guarantee fee (around 0.5% or less of the loan) which ultimately you pay as part of the loan cost. However, budget revisions have cut these fees significantly – as low as 0.37% per year for some loans – making borrowing cheaper overall.

Key benefits founders should know

- Easier Loan Approval: With CGTMSE guarantee, banks are more willing to approve loans. Many first-time entrepreneurs get funds who otherwise would be turned down for lack of collateral.

- Higher Loan Amounts: The guarantee limit has been raised (now up to ₹10 Cr per borrower). This means your small business can borrow more (e.g. for expansion) under the scheme than before.

- Lower Interest/Cost: Because the scheme reduces bank risk, you often get slightly better terms. Budget 2023 measures have cut the cost of credit by about 1%. Also, guarantee fees are discounted for lenders with good track records, which eventually benefits borrowers.

- Inclusion and Discounts: Women entrepreneurs, SC/ST founders, and other priority groups enjoy extra cover and fee discounts. For example, women-led firms get 90% coverage instead of 75%. This makes loans cheaper and more accessible for these groups.

- No Heavy Collateral: The big practical win – you can access bank credit without pledging buildings or fixed assets, at least for the guaranteed portion. For a young startup or a tech/service business without land, this is crucial.

- Boost to Credit History: Even though it’s a guarantee (not a subsidy), successfully repaying a CGTMSE-backed loan helps build a credit track record for your company. One CGTMSE tip: “Keep your repayments on track” to maintain ease of borrowing in future.

- Quick Processing for Smaller Loans: For loans up to ₹5 lakh, the paperwork is lighter (even PAN number is relaxed). This helps very small businesses get funds quickly. (For loans above ₹5 lakh, PAN and Udyam registration are mandatory.)

When this scheme makes sense

- Early-stage MSMEs: If you have a micro or small enterprise (even a startup) and need working capital or a small term loan, CGTMSE can be very useful. For a new unit with limited assets, the scheme makes banks give more weight to your business plan rather than seized collateral.

- Expansion or Purchase of Assets: When expanding or buying machinery, founders often need ₹10–50 lakh. Under CGTMSE, such loans can get guaranteed cover up to 75–85%, so banks may lend when they wouldn’t otherwise.

- No/Low Collateral: If your business lacks property (e.g. a cloud kitchen or a tech startup), applying under CGTMSE is a smart move. Even if you have some asset to pledge, the “hybrid model” lets the rest be guaranteed.

- Special Category Entrepreneurs: Women, SC/ST, PwD entrepreneurs especially benefit due to higher cover and fee benefits. If you belong to one of these groups, CGTMSE gives you an extra edge.

- Hesitant Lenders: If a bank is interested in lending but hesitant about risk, propose CGTMSE cover. Often, bankers will then approve your loan, knowing losses are insured.

In short, CGTMSE makes sense whenever a realistic, viable business (small size) struggles to get credit due to lack of guarantees. It is not limited to rural areas or specific industries – manufacturing shops, IT startups, shopkeepers, training institutes, even small transport operators can use it.

When this scheme may not be suitable

- Not for Large Projects: If your enterprise is medium or large (capital or turnover beyond MSME limits), it doesn’t qualify. CGTMSE is strictly for micro and small.

- Already Too Many Loans: If you already have multiple loans (especially ones that have defaulted), CGTMSE won’t help. Loans already in default or subject to earlier guarantee claims are ineligible.

- If Collateral is Plenty: If you have ample assets to pledge anyway, CGTMSE is less critical. Standard bank loans with collateral might offer better rates. Note however, fully collateral-backed loans are typically outside CGTMSE cover (except for the unsecured portion under the hybrid model).

- Business Not Viable/Risky: CGTMSE is not an automatic approval stamp. Banks still look at your business model, cash flows and the promoter’s track record. If your project is high-risk or not realistic, a bank can reject you with or without CGTMSE. The scheme doesn’t remove the need to show a solid business plan.

- Non-compliance or Illegal Activities: CGTMSE won’t cover loans that violate laws or RBI guidelines. For example, loans taken for banned activities or cases with legal issues are excluded.

- Documentation Gaps: If you lack essential documents (like Udyam registration, GST returns, PAN, etc.) your application can be rejected. In fact, from recent updates, having a Udyam number is mandatory for CGTMSE loans.

- Bank Isn’t Part of Scheme: Only loans from member lending institutions (MLIs) of CGTMSE are covered. If your bank or NBFC isn’t registered with CGTMSE, you cannot avail the guarantee. Always check that your lender is on the approved list of MLIs.

In essence, CGTMSE is not a free grant or foolproof program. It simply makes banks more comfortable lending to small business. Founders must still meet credit criteria (good credit history, financial statements, etc.) and cannot assume “automatic approval”. Banks retain full discretion to approve or reject even CGTMSE-backed loans.

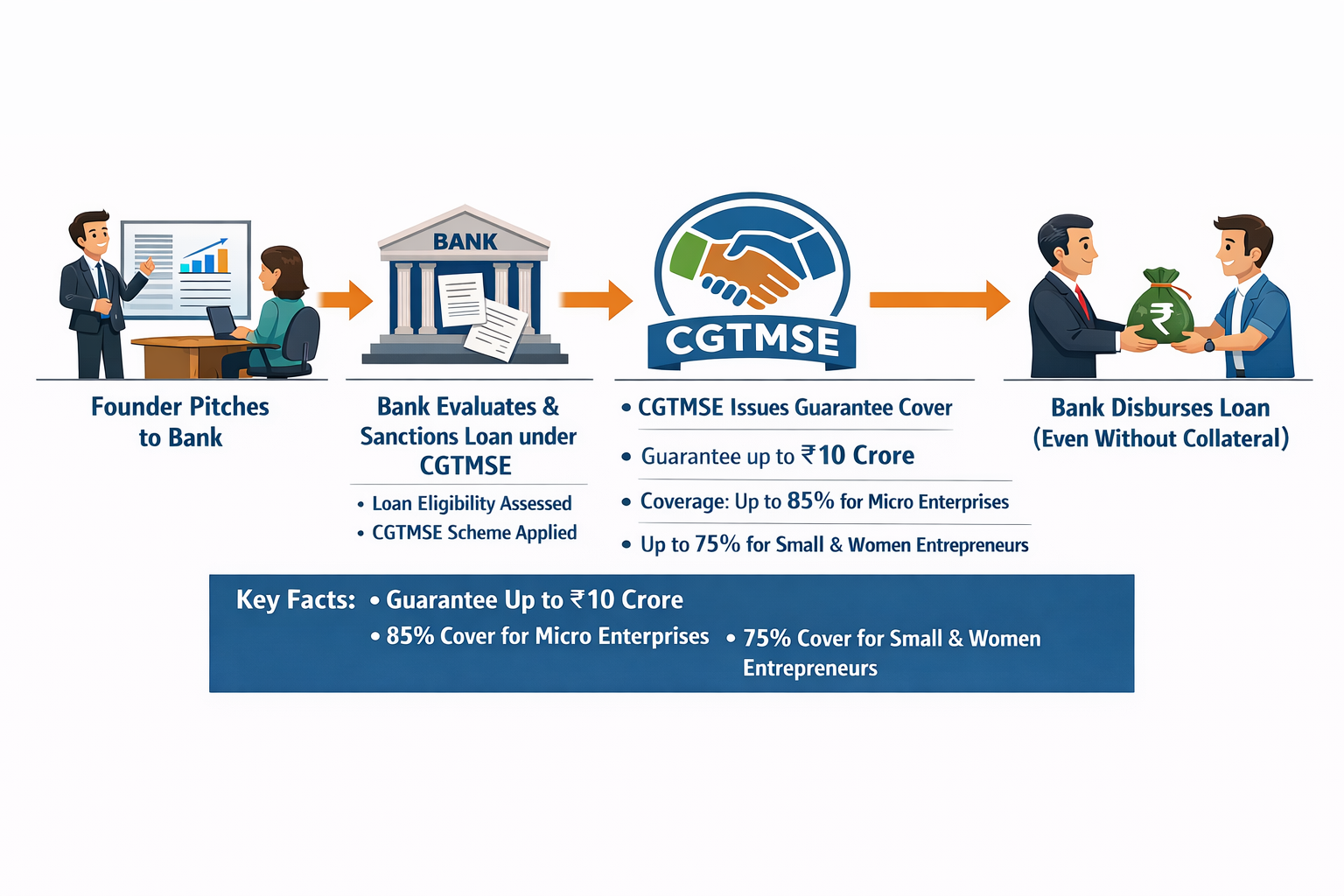

How the application process usually works

- Register and Prepare: First, ensure your business is formally registered (Udyam MSME registration is mandatory). Get your KYC docs ready: identity proofs, business plan or project report, financial projections, and basic licences.

- Choose a Member Bank (MLI): Go to a CGTMSE-registered lender – most public sector banks, private banks, NBFCs and even Microfinance Institutions are covered. You can check the official CGTMSE site for a list of MLIs.

- Submit Loan Application: Approach the bank with your loan application (term loan or working capital). Provide your business plan, financials, projections, Udyam number, and mention you want CGTMSE coverage. The bank will do its normal credit appraisal.

- Bank Sanctions the Loan: If the bank is satisfied, it sanctions/disburses the loan per its rules. Often, the loan is technically advanced first, then the guarantee is applied for – but in practice you’ll finalize guarantee before full disbursal.

- Apply for Guarantee: The bank then submits a CGTMSE application (usually online on CGTMSE portal) for your loan. The loan details and your business info (including Udyam number) go to CGTMSE along with a small guarantee fee payment by you (collected by the bank).

- Issue of Guarantee Cover: Once CGTMSE verifies details and receipt of fee, it issues a guarantee cover certificate to the bank. This formalizes the cover. After this, the bank has official risk cover on your loan.

- Loan Repayment: You repay the bank as usual. If all goes well, you never need to involve CGTMSE beyond payment of fee. If there is a default, the bank will invoke the guarantee (after following some recovery steps) and CGTMSE pays the guaranteed portion.

Keep in mind: The bank is your partner in this process. You cannot apply directly to CGTMSE – it must be via the lending institution. Always clarify with the bank which documents they need (usually business plan, identity, address, asset details, etc.) and remember to pay the guarantee fee on time. According to CGTMSE, keeping up timely payments on your loans is a “pro tip” to maintain smooth future access.

Common mistakes founders make

- Skipping Udyam Registration: Many first-timers forget MSME registration. But a valid Udyam number is now required for CGTMSE loans. Without it, your application can be rejected outright.

- Relying Solely on “Collateral-Free” Buzz: Some founders assume CGTMSE means no personal liability. Actually, while no property collateral is needed, banks typically still ask promoters to sign personal guarantees or board resolutions. Don’t be surprised if you still need to co-sign some documents.

- Weak Business Plan: CGTMSE helps on collateral, not on viability. If your financials or projections are sloppy, banks will reject even with CGTMSE. Present a clear, realistic plan.

- Underestimating Paperwork: CGTMSE requires specific forms and KYC. Missing details like PAN, GST, or certificates of incorporation can delay or derail the process. Always check the CGTMSE checklist with your bank.

- Ignoring Bank’s Discretion: A guarantee isn’t an entitlement. If the bank’s credit officer isn’t convinced about the business, they won’t lend. Founders sometimes mistake CGTMSE as a “sure thing” – it isn’t. Always prepare as if you’re pitching for a normal loan.

- Failing to Track Repayments: If a CGTMSE-backed loan goes bad (NPA), you may lose future trust eligibility and hurt credit rating. In fact, accounts that slip to NPA too quickly (within 90 days) cannot be claimed. Keep your loan repayments on time to avoid complications.

- Ignoring Hybrid Model Limits: For partially secured loans (hybrid), founders sometimes assume the entire loan will be covered. Actually, CGTMSE only covers the unsecured portion. Verify how much of your loan will be guaranteed, and ensure you can repay the rest.

By avoiding these mistakes – and working closely with the lending bank – founders can make the best use of CGTMSE. Remember, the scheme is a tool to reduce risk, but it requires good documentation and responsible repayment to succeed.

Official source & verification

Always cross-check CGTMSE details with official sources. The CGTMSE website (cgtmse.in) has scheme documents, circulars and FAQs. For example, the site notes that the guarantee cover ceiling is now ₹10 crore and fees have been reduced. Government press releases and budget documents also confirm key updates (e.g. Budget 2023 announcements on infusion of ₹9,000 cr and ₹2 lakh cr new credit). To verify eligibility or process steps, consult the official CGTMSE FAQ pages and the Ministry of MSME communications. In short, trust but verify with the CGTMSE and MSME ministry resources rather than relying only on third-party summaries.

FAQs

Q1: What exactly is the CGTMSE scheme?

A1: CGTMSE stands for Credit Guarantee Fund Trust for Micro and Small Enterprises. It’s a partnership between the government and SIDBI to help small businesses get loans. Under CGTMSE, banks can lend to eligible MSEs without insisting on collateral or personal guarantees. Instead, if the loan defaults, the CGTMSE fund covers most of the loss (up to 75–90% of the loan, depending on borrower category). This “loan insurance” encourages banks to finance startups and small enterprises. The scheme has been revamped with a larger corpus (₹9,000 cr infusion) to support much more credit (an extra ₹2 lakh cr) and lower interest costs.

Q2: Who can apply for a CGTMSE-backed loan?

A2: Any new or existing Micro or Small Enterprise in manufacturing or services can apply. This includes sole proprietors, partnerships, LLPs, and private companies, as long as they have MSME (Udyam) registration. The scheme excludes agriculture, SHGs and certain other categories. Importantly, startups also qualify if they are registered as MSMEs. Check with your lender that you fall under the MSE definition and have your Udyam number ready, since that’s mandatory now.

Q3: How much loan can I get and what percent is guaranteed?

A3: The maximum loan amount that CGTMSE covers is now ₹10 crore per borrower. Within that, the trust guarantees a percentage of the loan outstanding in case of default. Typically, 75% of your loan is covered. Certain borrowers get higher cover: for women entrepreneurs and Agniveers, it’s 90%, and for SC/ST, PwD, ZED-certified units, etc., it’s 85%. If your business is in an identified credit-deficient district, you get an extra 5% on top of those rates. You should plan on paying the remaining portion yourself if a claim happens. In practice, this means banks feel safe lending you up to that coverage limit without requiring your assets as security.

Q4: Do I need to provide collateral or personal guarantee?

A4: For loans under CGTMSE, no property collateral or third-party guarantee is generally required for the guaranteed portion. The scheme’s whole point is to allow “collateral-free” (in effect) credit. However, banks often still ask entrepreneurs to sign personal guarantees or board resolutions – so you may have some personal liability – but they won’t seize your factory or land as collateral. Under the hybrid security model, if part of the loan is secured by collateral, CGTMSE will guarantee only the unsecured portion up to ₹10 cr. Always clarify with your bank: the idea is to minimize, not necessarily eliminate, your own asset pledge.

Q5: What is the hybrid collateral model?

A5: The hybrid model is a new option for partly secured loans. In this, the lending bank takes collateral (like equipment or property) on part of the loan, and CGTMSE covers the rest. For example, if you need ₹50 lakh and have ₹20 lakh worth of equipment to offer, the bank might take that as collateral for ₹20 lakh of the loan, and CGTMSE could guarantee the remaining ₹30 lakh (within the ₹10 cr limit). This “partial collateral security” scheme ensures that even businesses with some assets get the benefit of guarantee on the unsecured portion. So CGTMSE is not only for completely asset-less loans; it can complement your own collateral to make banks comfortable lending more.

Q6: How do I apply, and where can I verify details?

A6: You apply through a member lending institution (MLI) – that is, a bank or NBFC registered with CGTMSE. First, talk to your bank about a loan and mention CGTMSE. Once the bank approves and disburses the loan (subject to its credit appraisal), the bank will apply to CGTMSE for guarantee cover. You will need to submit KYC docs (PAN, Aadhaar, business registration, Udyam certificate, financials) and pay a small guarantee fee to the trust. The official CGTMSE website (cgtmse.in) has guides and application forms. You can verify all rules and updates there or via the MSME Ministry releases. Remember, approval is not automatic – both your bank and CGTMSE must accept the application.

Read More Blog-Stand-Up India Scheme

Eligibility Criteria

Registered MSMEs, Retail traders, SHGs, Educational institutions

🚀 Ready to Scale Up?

Don't miss this opportunity! Visit the official portal to check your eligibility and apply today.

Apply Now on Official Website →

Comments are closed