Subtotal $0.00

BenefitCollateral-free loans ₹1 lakh (1st tranche, 18 months) + ₹2 lakh (2nd tranche, 30 months) at 5% interest; ₹15,000 toolkit incentive; ₹1/digital

Valid Till31 Dec, 2028

Scheme CodeCVS 2023

PM Vishwakarma Scheme: A Practical Guide for Artisans and Small Founders

Intro: The PM Vishwakarma Kaushal Samman Yojana (PM Vishwakarma Scheme) is a government initiative launched on 17 Sept 2023 to help India’s traditional artisans and craftsmen. It aims to bridge gaps in the largely informal crafts sector by providing formal support: training, recognition, tool grants, and easy credit. As a first-generation artisan-founder, you care about this scheme because it offers subsidised loans, skill upgrades, and market support that can help grow your craft business sustainably. The scheme understands that artisans often lack formal financing or digital networks; it tries to fix that by onboarding you to banking and digital services. In short, PM Vishwakarma is a bank-loan opportunity with support, not a giveaway – it can boost your trade if you qualify and prepare properly.

What is this scheme?

PM Vishwakarma is a Central Government scheme for artisans and craftspeople. Officially called the Pradhan Mantri Vishwakarma Kaushal Samman Yojana, it was launched by the Prime Minister in Sept 2023 to provide “end-to-end support” to artisans working with traditional tools. In practice, that means recognition, training, and subsidised loans up to ₹3 lakh – all in stages. The government has allocated about ₹13,000 crore for five years (FY24–28) to implement it. Unlike a pure grant, this scheme’s core is credit and self-reliance. It partners with banks and Common Service Centres (CSCs) to register beneficiaries, offer Aadhaar-based eKYC, and disburse funds. It also connects artisans to formal MSME registration (Udyam) and online platforms for marketing. But remember: the final credit approval is by banks, not guaranteed by the government portal.

Who is this scheme for?

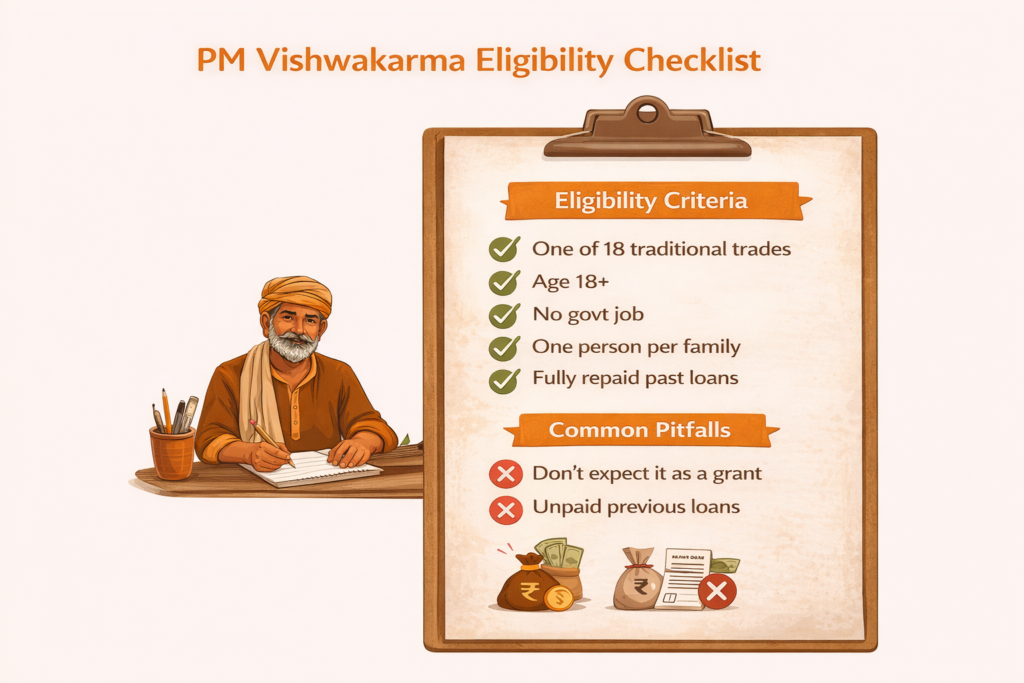

PM Vishwakarma is only for traditional artisans and craftsmen working with their hands and tools, on a self-employed basis. It covers 18 specific trades (e.g. carpenter, blacksmith, goldsmith, potter, sculptor, cobbler, mason, basket-weaver, barber, tailor, washerman, fishing-net maker, etc.). To be eligible, you must be 18 or older and actively practicing one of these family-based trades on the date of application. The scheme is one-person-per-family: only one member in the family (husband, wife, unmarried children) can enroll. Government employees and their families cannot apply. Also, you should not have taken a similar government credit scheme (like PMEGP, MUDRA, PM SVANidhi) in the past five years unless that loan is fully repaid. These rules ensure the benefits reach eligible artisans fairly across communities.

What support does it offer?

PM Vishwakarma provides a bundle of support tailored for artisans:

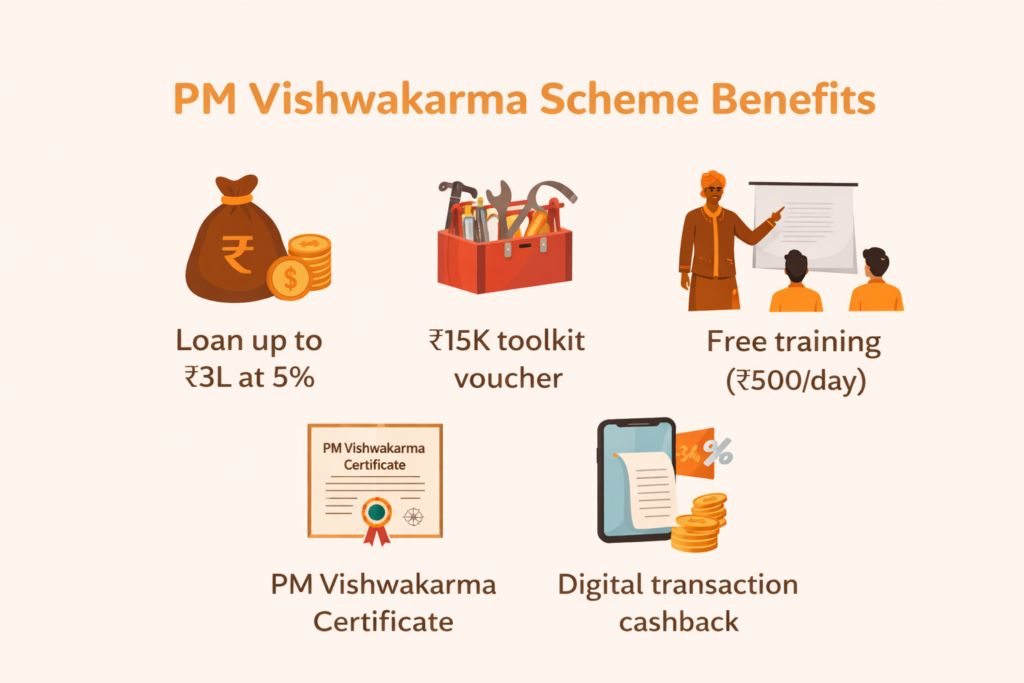

- Recognition: Every registered artisan gets a PM Vishwakarma certificate and ID card, officially recognizing their skill. This can build trust with customers and institutions.

- Skill Training: The scheme funds basic and advanced training. You can get 5–7 days of basic training plus 15+ days of advanced training in modern or advanced techniques, along with a stipend of ₹500 per day during training. This helps you improve your craft and learn new business skills.

- Toolkit Grant: At the start of basic training, you receive e-vouchers worth up to ₹15,000 to buy new or modern tools for your trade. This cuts your upfront investment in equipment.

- Collateral-Free Loan: The core is a cheap bank loan of up to ₹3 lakh (₹1 lakh + ₹2 lakh in two stages) for your artisan business. This ‘Enterprise Development Loan’ has a concessional 5% interest rate (government pays about 8% of the cost). No collateral is required. The first ₹1 lakh tranche becomes available after you complete basic training. The second ₹2 lakh tranche can be taken only after the first loan is used responsibly (maintaining accounts, adopting digital payments) or after you undergo advanced training. Both tranches have fixed tenures (18 and 30 months respectively).

- Digital Incentive: To encourage digital payments, the scheme credits ₹1 to your bank account for each digital transaction (up to 100 per month). This effectively rewards you with “free” money for switching to online payments in your business.

- Marketing Support: The government will help with marketing efforts – things like quality certification, branding, listing on platforms (e.g. Government e-Marketplace), publicity and online advertising. This aims to expand your market reach beyond local customers.

- Formalisation: On joining, you’re also listed on the Udyam Assist Portal as an MSME entrepreneur. This helps in getting future benefits meant for small businesses and shows you as a registered enterprise.

All of the above is administered through an online portal via CSCs: you register at a Common Service Centre with Aadhaar-based eKYC, then undergo local verification before approval. In essence, the scheme offers you training and tools to improve your craft, plus an easy loan to invest in your work, under supportive government oversight.

Key benefits founders should know

For first-gen artisans, the PM Vishwakarma Scheme can be a game-changer if used wisely. Important benefits include:

- Low-cost credit: A ₹3 lakh collateral-free loan at just 5% interest is rare for small unregistered businesses. This can finance new equipment, raw materials or even an extra hand at work.

- Modern tools via voucher: The ₹15,000 e-voucher fills the gap when you can’t afford modern tools upfront. Up-to-date tools increase productivity and product quality.

- Skill upgrade & stipend: Free training with a daily stipend (₹500) not only hones your craft but also lets you earn while learning. Improved skills can help you command better prices.

- Government recognition: The PM Vishwakarma ID card can boost credibility. It signals your official artisan status when dealing with customers or institutions.

- Digital habits & small rewards: The ₹1-per-digital-transaction incentive (up to ₹100 a month) is a smart way to nudge businesses online. Even small digital earnings add up while making transactions traceable.

- Marketing push: Branding and e-commerce support help you tap wider markets (even urban or export markets) that you normally can’t reach. Over time, this can mean more orders and higher earnings.

- Formal MSME identity: Getting on the Udyam register can open doors to other schemes, tenders, and recognition as a formal business, beyond just a casual artisan.

These benefits, taken together, mean you can modernize your practice and access credit as if you were a small factory, not just a lone artisan. The scheme is specifically built to lower barriers (no collateral, online registration) and add value (training, marketing) to traditional trades.

When this scheme makes sense

PM Vishwakarma is most useful if you are a dedicated artisan/craftsman with a clear plan to grow your trade. It makes sense when:

- You need capital for tools, raw materials, or to hire an assistant, and your needs are within ₹3 lakh.

- You are willing to undergo basic training and start using digital payments.

- You want to officially register your craft business as an MSME (through Udyam).

- You have a real small business plan (e.g. turn raw clay into pottery products) and can explain how you will repay a bank loan.

- You value government recognition and broader market access via branding or e-commerce.

- You have had no recent government business loan (or fully repaid any you had).

- You are an early-stage or small artisan enterprise (even home-based) that wants to become more formalized.

In short, it’s ideal for entrepreneurial artisans who are serious about improving their work, learning new skills, and accessing formal credit. It especially benefits first-generation craft businesses who often struggle to get bank loans on their own.

When this scheme may not be suitable

PM Vishwakarma is not for everyone. It may not suit you if:

- Your trade is not one of the 18 specified categories (e.g. electricians, textile weavers, or large industrial craftsmen are outside scope).

- You don’t meet the eligibility (under 18, non-artisan job, already took a government loan and didn’t repay it, or you’re a government employee).

- You don’t want to attend training or deal with digital processes (digital transactions are mandatory for second loan).

- You need a grant or subsidy rather than a loan (this is a repayable loan scheme).

- You expect quick cash with no follow-up: bank approvals take time, and you must stick to repayment schedules.

- Your family already got benefits (remember one-per-family rule).

- You want more than ₹3 lakh – note the total cap is ₹3L, which may not be enough for very capital-intensive crafts.

- You have no realistic plan for using the money profitably.

Be practical: if you’re not prepared to manage a formal loan (even with help), or your needs far exceed ₹3L, consider other options too. Also, timeline-wise, it can take weeks or months from registration to first loan, because banks will assess your credit proposal. So this scheme is best if you are patient and organized, not if you need instant cash.

How the application process usually works

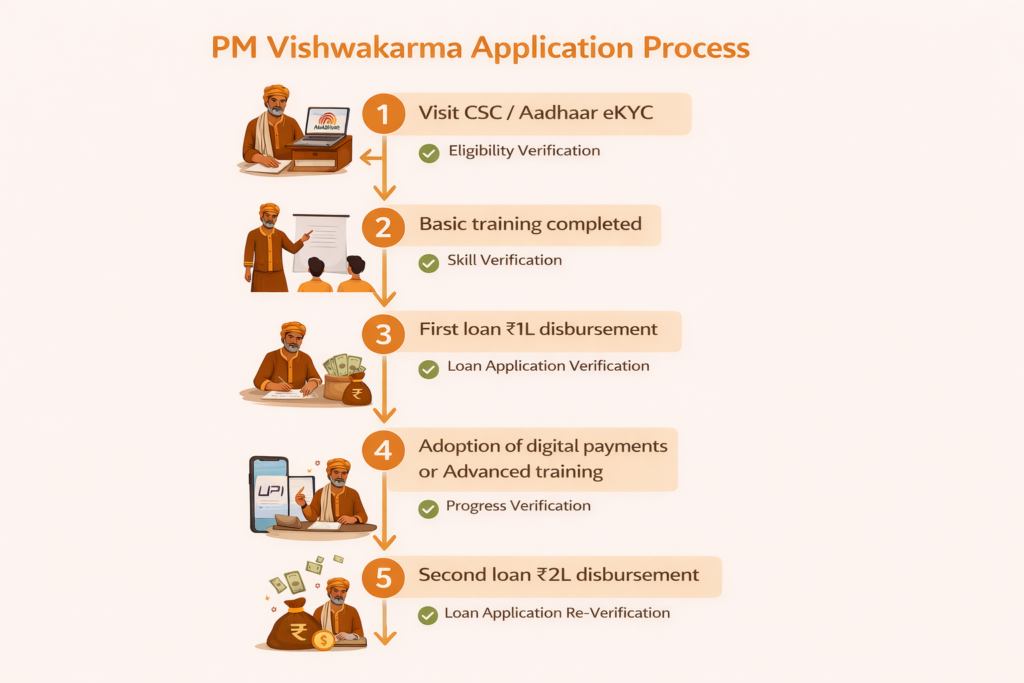

- Registration via CSC: Go to a nearby Common Service Centre (CSC). An operator will use your Aadhaar (Aadhaar-based biometric eKYC) to register you on the PM Vishwakarma portal. You’ll fill basic details and trade info.

- Local verification: After registration, local authorities verify your application in three steps (village or city level, district committee, final screening). This can take time – make sure to follow up.

- Training enrollment: Once approved on paper, you get details of free training sessions. Attend and complete the 5–7 day basic training. You’ll get ₹500/day stipend during this.

- Toolkit e-voucher: At the start of training, you receive e-vouchers (up to ₹15,000) which you can redeem for tools or equipment from approved sellers. This typically happens via CSC or designated vendors.

- Loan application – first tranche: After basic training, you become eligible for the first loan of ₹1 lakh. At this point, approach a bank branch (preferably one offering MSME loans, e.g. nationalized banks or RRBs). You’ll present your PM Vishwakarma ID and business plan. The bank will verify your application. Under the scheme, the loan will be at 5% interest without collateral.

- Maintain records: Once you get the first loan, use it wisely for your business and keep clear accounts. Also start using digital payments (UPI, cards etc.) in your business, to earn that Re.1 incentive per transaction. This builds a track record for you.

- Advanced training (optional) & loan – second tranche: If you want more funds, either complete the 15+ day advanced training or continue good digital payment habits. Then you can apply for the second tranche of ₹2 lakh. Again, meet the bank with your records to get this loan. By now you have training certificates and a first-loan repayment record to support you.

Throughout, you can check the PM Vishwakarma portal (or ask the CSC) to track status. The scheme office may also push helpful communications or eKYC prompts. Remember, the portal and CSC help you get connected; the bank actually approves loans. So be ready with documents like identity proof, address proof, trade proof (if any), and a simple project report. It often helps to bring your bank passbook and PAN card too.

Common mistakes applicants make

- Treating it as free money: This scheme is a loan program, not a grant. Some applicants mistakenly believe they will get cash without repayment. In reality, you must repay the bank (at 5% interest). Plan carefully and make sure you can pay back the installments.

- Skipping preparation: Many ignore preparing a basic project report or business plan. Lenders expect a clear use of funds. Don’t go with empty hands – even a simple note on what you’ll buy and how you’ll earn back will help your case.

- Wrong assumptions about approval: Registering on the portal does NOT guarantee loan approval. Some artisans think filling the form means money is automatic. Actually, banks will still screen your loan request like any other. The PM scheme only lowers barriers; it doesn’t bypass bank rules.

- Avoiding digital transactions: Forgetting the digital payment requirement can cost you. If you don’t start accepting digital payments (UPI, etc.), you may be ineligible for the second loan tranche. Keep small digital receipts to show.

- Ignoring eligibility details: Overlooking the one-per-family rule or prior-loan restrictions can lead to rejection. Check that no family member has already taken the scheme benefit, and that your last big loan (if any) is fully repaid. Similarly, if you’re a government employee (or spouse), the scheme isn’t for you.

- Delayed follow-up: Waiting quietly after registration is risky. You should follow up with CSC or district offices to ensure verification steps are done. Many applicants drop out simply because they assume “no news = rejection” without checking.

- Choosing the wrong bank: Some go to any bank branch and get turned away if that branch isn’t dealing with the scheme. It’s best to approach a branch of a nationalized bank or an RRB that offers MSME loans under this scheme. Asking at your local bank or the CSC can guide you.

By avoiding these mistakes, your application stands a much better chance. Always double-check the official guidelines or ask the scheme helpline if unsure – misinformation can waste time and effort.

Official source & verification

For accurate and updated details, always refer to official sources. The Ministry of MSME website and press releases provide authoritative info. For example, the PIB press release and guidelines list all benefits and terms. The official PM Vishwakarma portal (pmvishwakarma.gov.in) has the registration link and FAQs. It’s recommended to verify key points there or through the toll-free helpline 1800-267-7777 (also announced in MSME communications). Avoid relying on unofficial social media posts or agents; only the government site and CSCs are legitimate channels. Before you apply, read the “Guidelines” PDF (available on the portal) or printed pamphlets from MSME offices, so you know exactly which documents and conditions apply.

FAQs

- Who can apply for PM Vishwakarma Scheme?

Any self-employed artisan or craftsperson (age 18+) working in one of the 18 specified traditional trades (like carpenter, blacksmith, potter, etc.) can apply. You must not be a government employee, and only one person per family can join. Also, if you’ve availed a government self-employment loan (like Mudra or PMEGP) in the last 5 years, you’re ineligible unless that loan is fully repaid. - What benefits do I get under this scheme?

If approved, you get a PM Vishwakarma ID/certificate, free basic and advanced training (with ₹500/day stipend), up to ₹15,000 in tool vouchers, plus a low-interest loan (up to ₹1L first tranche, ₹2L second tranche). You also earn ₹1 for each digital transaction (up to 100 per month) and receive marketing support (certification, branding, e-commerce help). Essentially, it’s recognition + training + financial support (loan) to boost your craft. - Is the loan collateral-free and what is the interest rate?

Yes, the loans under PM Vishwakarma are collateral-free. The interest rate is a concessional 5% per year. The government pays roughly 8% of the normal interest cost as a subsidy, so you effectively pay only 5%. You need to repay the loan in installments, but there’s no security (like property) required, which is great for small artisans. - Do I need to pay any application fee or margin money?

No, there is no application fee or up-front contribution required by the scheme itself. You won’t be asked to invest your own money (“margin money”) for this loan. However, banks may check your ability to repay, so you should be prepared to show some savings or income. But technically, the scheme’s loan is fully funded by the bank with government guarantee, so you shouldn’t pay a margin upfront. - How do I apply and where?

Visit your nearest Common Service Centre (CSC) with your Aadhaar and basic documents. The CSC operator will register you on the PM Vishwakarma portal and help with verification. After approval and training, you approach a designated bank branch for the loan. You can find application instructions on the official portal (pmvishwakarma.gov.in) or ask at the MSME District Office. Remember to carry ID proof, address proof, and any details of your trade. - If I already have a MUDRA loan, can I still apply?

If you have taken a MUDRA or PM SVANidhi loan in the past 5 years and it is not fully repaid, you are ineligible for PM Vishwakarma. But if you fully repaid those loans, you can apply. The idea is to not overlap benefits for the same purpose. Always clarify with bank officials if unsure. - How long does it take to get the loan?

It varies by district and bank. Typically, registration and verification may take a few weeks. After you complete the basic training, getting the first loan could take anywhere from a month to two months, depending on how quickly you and the bank process paperwork. The second loan (₹2 lakh) comes after you have the first loan account in order and either adopted digital payments or finished advanced training. Plan on weeks to months rather than days – good projects and patience pay off here.

Read More Blog-CGTMSE Scheme 2023

Eligibility Criteria

Artisans in 18 traditional trades (self-employed, 18+)

🚀 Ready to Scale Up?

Don't miss this opportunity! Visit the official portal to check your eligibility and apply today.

Apply Now on Official Website →

Comments are closed