Subtotal $0.00

Email : 23

BenefitCollateral-free loans: Shishu (₹50K), Kishore (₹50K-₹5L), Tarun (₹5L-₹10L), Tarun Plus (₹10L-₹20L)

Valid Till31 Dec, 2030

Scheme CodePMMY 2015

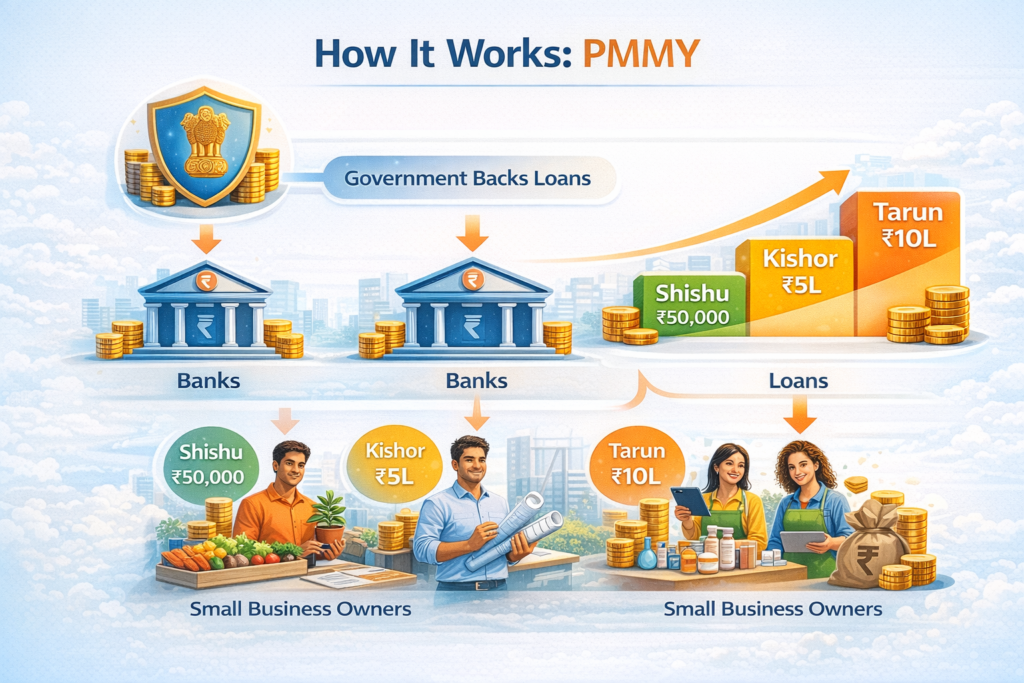

Launched in April 2015, PMMY is a flagship scheme to boost micro and small enterprises by providing easy bank credit. It is not a grant but a government-backed loan program that helps “fund the unfunded” in the informal sector. Under PMMY, loans up to ₹10 lakh (now raised to ₹20 lakh) are available across three tiers – Shishu, Kishor, and Tarun – reflecting business growth stages. The scheme is run by MUDRA (Micro Units Development & Refinance Agency Ltd.), which refinances banks and extends credit guarantee so that banks lend easily to micro-entrepreneurs.

Who It’s For

PMMY targets non-corporate, non-farm micro and small businesses. Eligible ventures include individual proprietors, partnerships or small companies in manufacturing, trading and services. Typical beneficiaries are shopkeepers, artisans, repair shops, food stalls, transport operators, service centres, etc., often in Tier 2–Tier 6 towns. Allied agri activities (like poultry, dairy, beekeeping) are also covered. Women entrepreneurs and SC/ST/OBC founders are major focus areas, but any Indian citizen with a viable small-business plan can apply.

How It Works

PMMY is a repayable loan scheme, not a grant. Banks and NBFCs issue loans, while the government (via MUDRA/CGTMSE) provides refinancing and guarantee, ensuring loans are collateral-free or low-collateral. Loans are unsecured up to ₹10 lakh (per RBI rules) and now up to ₹20 lakh under the new Tarun Plus category. Importantly, approval rests with the lender – government only backs the loan, it does not directly sanction or disburse funds. Borrowers repay the loan with interest; the interest rate is set by the bank (often in the 8–12% range).

The three core categories are:

- Shishu (Up to ₹50,000): For entrepreneurs in idea/early stage or with minimal capital needs.

- Kishor (₹50,001 – ₹5,00,000): For growing businesses needing working capital or equipment.

- Tarun (₹5,00,001 – ₹10,00,000): For established micro-enterprises seeking larger expansion or scaling.

(A new “Tarun Plus” ₹10–20 lakh tier was added in 2024 for borrowers who successfully repaid a Tarun loan.)

Eligibility & Documentation

Basic criteria: Applicant must be an Indian citizen (age 18–65) running or proposing a non-farm income-generating enterprise. Business structures can be sole proprietorships, partnerships, or companies. The business must have formal registration (e.g. trade license, GST/Udyam/MSME registration if applicable) and a bank account. GST registration is not mandatory for small (Shishu) loans, but the business should at least have basic registration or license. A clear business plan or project outline is essential – lenders look for viability and repayment strategy. Most banks also require a decent credit history (no past loan defaults).

Required documents typically include: identity proof (Aadhaar/PAN/passport), address proof, photographs, business proof (license, Udyam/MSME certificate or shop act registration), bank statements (last 6–12 months), and basic financials (ITR or balance sheet for loans above ₹2 lakh). You may also need quotes for machinery or equipment if funding assets, and category certificates (SC/ST/OBC/minority) if claiming concessions. Udyam (MSME) registration is not mandatory for application but can be obtained for benefits later; you can apply for the loan on the Udyamitra portal before formal Udyam registration. Ensure all KYC details (name/address) exactly match your Aadhaar and ID documents.

Benefits and Use Cases

Key benefits: Mudra loans are collateral-free and cost-effective for small businesses. There are no processing fees for Shishu loans (and nominal fees for higher tiers). Government backing increases lender confidence and may even yield a small interest concession for priority groups (e.g. 0.25% concession for women entrepreneurs in some banks). Loan amounts (₹50,000–20 lakh) are flexible, making this scheme suitable for diverse uses – from buying a sewing machine, shop setup, inventory purchase, vehicle purchase, to expanding a small factory or service unit.

Practical examples: A new food cart or vegetable vendor could use a Shishu loan for equipment and initial stock. An existing bakery might use a Kishor loan to buy a larger oven and ramp up production. A small tailoring unit might take a Tarun loan to open a second shop or install new machinery. In short, PMMY is well-suited when your business needs moderate capital and you prefer structured bank finance over informal lenders.

When to apply: Consider PMMY early in your startup journey or at clear expansion points. It makes sense if you have a concrete small business plan, need funds up to ₹10 lakh (up to ₹20 lakh for Tarun+), and can repay over 1–5 years. Unlike venture capital, this is not for high-risk innovation projects or funding R&D. It’s best for ventures that generate steady cash flows and can service debt. Since the scheme aims at financial inclusion, first-time borrowers or those with limited collateral will find it particularly useful.

Limitations & Who It’s NOT For

PMMY is not a fit if you’re seeking grant, equity, or financing beyond ₹20 lakh. It’s not intended for large or speculative ventures. For example, crop farming is excluded (though allied activities like dairy or poultry qualify). Personal expenses or non-business uses are strictly out of scope. Similarly, businesses with existing big loans, poor credit history, or no realistic plan may face rejection. If your enterprise is already well-funded by VC/angel investment, or requires very large capital, PMMY might not help. In essence, don’t approach Mudra expecting “free money” or an instant grant: you will need to repay, and banks will judge you like any borrower.

Application Process & Approval

Step 1 – Prepare: Craft a simple project report/business plan with cost estimates. Get basic business registration (shop license, partnership deed, etc.) and KYC docs ready. Obtain Udyam registration if possible (though not strictly required at application).

Step 2 – Apply: You can apply online or offline. For online, use the government portals: UdyamiMitra or JanSamarth. These let you select loan category (Shishu/Kishor/Tarun), fill forms, and upload documents. The portal then matches you with participating lenders. Alternatively, go in-person to any participating bank/NBFC branch (public/private banks, MFIs, regional rural banks, small finance banks) and request a Mudra loan form. Attach the same documents and your plan.

Step 3 – Bank Processing: The bank will review your application, KYC, and business plan. They may ask further questions or require clarifications. If the bank is convinced of your viability, they sanction the loan. The disbursement can be lump sum or phased depending on project needs. From application to disbursal can take several weeks, so patience and follow-up are key. Note: submitting on the portal or to the bank is not a guaranteed approval – banks use their credit criteria and can reject if gaps exist.

Common Mistakes & Tips

- Weak Business Plan: Never apply with just an idea. Prepare a clear plan explaining how you will use the funds and repay. Include basic numbers (project cost, sales, profit estimates).

- Wrong Category: Pick the loan category that matches your current business size. Applying for Tarun with a tiny venture can be refused; similarly, underestimating your need (applying in Shishu when you need ₹4 lakh) can cause multiple loans or rejections. Lenders expect logical justification of loan amount.

- Incomplete Documents: Double-check KYC details. Ensure your Aadhaar, PAN, and bank statements match your application exactly. Missing proofs or mismatched names/addresses often delay or derail the process.

- Unrealistic Expectations: Remember this is a formal loan. Do not treat it as “free money.” Avoid over-optimistic revenue projections just to impress the bank. Show realistic, conservative figures.

- Single Source Dependence: Relying only on portals can be a mistake. Also reach out directly to banks (especially those active in MSME lending). Sometimes local branch managers can guide you or expedite the process better than just online submission.

By preparing thoroughly, choosing the right category, and presenting a sound plan, founders greatly improve their Mudra loan chances.

Conclusion

PMMY is a powerful financing tool for Indian micro-entrepreneurs when used wisely. It provides structured bank credit (with government support) for businesses that often struggle to get institutional loans. Founders should approach it like any loan: with planning, diligence, and clear repayment strategy. It won’t cover deep tech or high-risk startups, nor is it an entitlement. But for a small shop, workshop or rural enterprise that needs affordable capital up to ₹10–20 lakh, PMMY can unlock growth and livelihood opportunities. Always verify details (and any updates) on the official Mudra or UdyamiMitra portals, and remember that final approval lies with the lending bank.

Read More Blog-How Founders Can Avoid Burnout Using AI Productivity Tools

Eligibility Criteria

Individuals, SHGs, Proprietorship, Partnership, Private Ltd, Micro/Small enterprises

🚀 Ready to Scale Up?

Don't miss this opportunity! Visit the official portal to check your eligibility and apply today.

Apply Now on Official Website →

Comments are closed