Subtotal $0.00

Email : 10

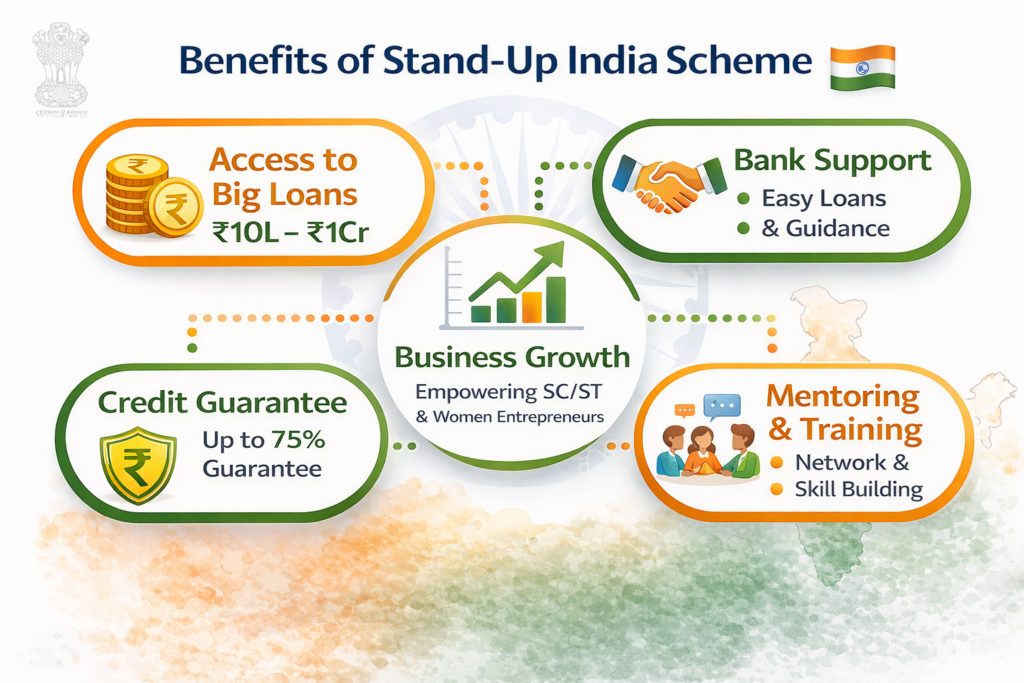

BenefitBank loans ₹10 lakh to ₹1 crore; margin up to 15%; interest subvention available

Valid Till31 Dec, 2030

Scheme CodeSUI 2016

Stand-Up India Scheme: A Founder’s Guide to Loans for SC/ST & Women Entrepreneurs

The Stand-Up India Scheme is a loan program for India’s new entrepreneurs from SC, ST and women communities. If you’re a first-time founder in these groups, this scheme offers you a chance to get bank loans (₹10 lakh–₹1 crore) with government support. It matters to founders because it unlocks funding that might otherwise be hard to find. Banks back your greenfield (new) business with this loan, along with guidance on business planning. But remember: this is a loan, not a grant – you must repay it, and banks make the final call on approval. The scheme has already helped over 1.8 lakh entrepreneurs (80% of whom were women) gain capital for their startups.

What is this scheme?

Stand-Up India was launched on April 5, 2016, by the Government of India to boost entrepreneurship among Scheduled Caste (SC), Scheduled Tribe (ST) and women entrepreneurs. It aims to create an ecosystem supporting these founders with easier access to finance. Under the scheme, banks provide loans from ₹10 lakh up to ₹1 crore for setting up a greenfield (new) enterprise in manufacturing, services, trading or allied agricultural activities. Every bank branch is encouraged to lend to at least one SC/ST entrepreneur and one woman entrepreneur under this scheme. The Stand-Up India portal (StandUpMitra) and local bank managers help entrepreneurs with training and loan applications.

Who is this scheme for?

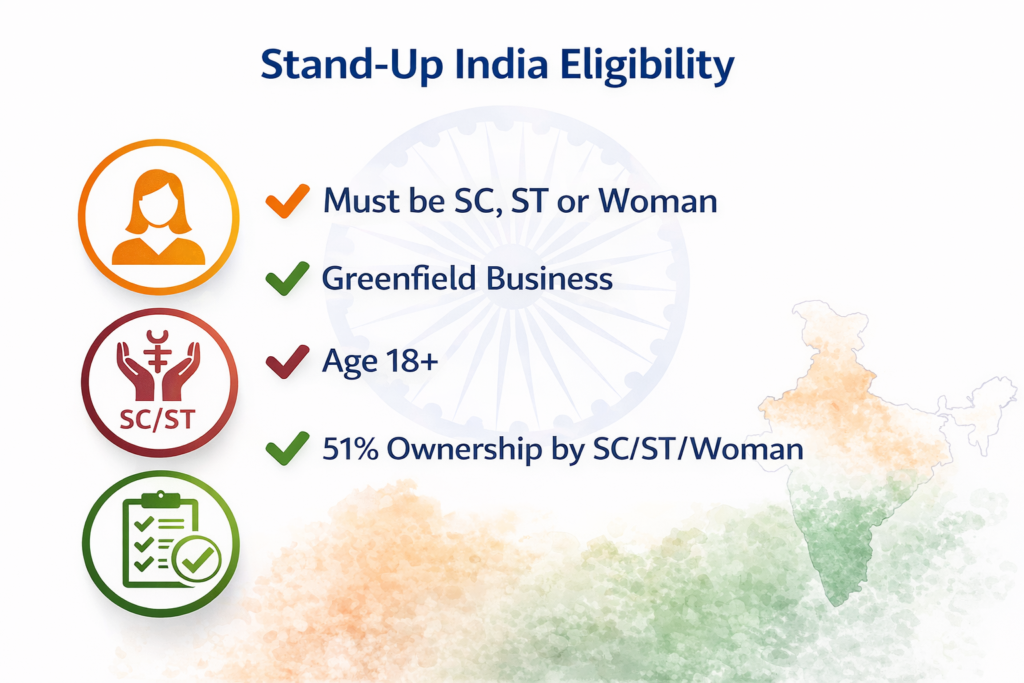

The scheme is strictly for first-time (greenfield) entrepreneurs in the target groups. Eligible founders are:

- Individual SC or ST candidates, or any woman entrepreneurs, aged 18+.

- Or companies/LLPs where majority ownership (≥51%) and management is held by SC/ST and/or women entrepreneurs.

- The venture must be non-farm (so farming/crop loans don’t qualify) and brand-new (you haven’t set up a similar business before).

- Borrowers must not be defaulters on any other bank loan.

Example: A 25-year-old Dalit woman starting her first textile manufacturing unit qualifies. If she co-founds a company, she needs to hold at least 51% stake.

What support does it offer?

Loans with government backing: Qualified founders can borrow ₹10 lakh to ₹1 crore from any scheduled bank. These loans cover project costs and some working capital. Banks apply normal lending rates (roughly MCLR + up to 3%). There’s no special interest subsidy, but the loan often comes with CGTMSE credit guarantee (so you pay a small premium instead of full collateral). Up to 15% of project cost can be covered by “margin money” support under other govt schemes, and you must invest at least 10% of the project cost as your own contribution.

Handholding & training: Beyond money, the scheme provides support. The StandUpMitra portal (run by SIDBI) offers step-by-step guidance—from preparing a project report to filling loan applications. Over 8,000 agencies (like entrepreneurship cells, skilling centers, mentors) help you polish your plan and get ready to pitch to the bank. Banks also issue a RuPay card to withdraw the sanctioned credit, and they keep track of your loan usage so funds are used for business needs.

Refinance and guarantees: Government has allocated funds for this scheme. SIDBI got a ₹10,000 crore fund for refinancing these loans. The National Credit Guarantee Trustee Company (NCGTC) has a ₹5,000 crore corpus to back these loans, so in practice banks get a substantial guarantee cover. This usually means no collateral for loans up to ₹10 lakh (as per general small-loan rules), and reduced collateral requirements for larger loans. Dr. Milind Kamble (DICCI chief) notes this scheme has given collateral-free loans from ₹10L to ₹1Cr to thousands of SC/ST entrepreneurs.

Key benefits founders should know

- High loan amounts: You can secure up to ₹1 crore, which is often more than other schemes like PM MUDRA (max ₹10 lakh).

- Targeted to you: Banks are expected to lend one loan each to an SC/ST and a woman entrepreneur per branch, so branches have a quota. In effect, there’s institutional will to approve suitable applications.

- Guidance support: The free StandUpMitra portal and LDMs (Lead District Managers) help you with paperwork and training. You don’t have to navigate alone.

- Credit guarantee: With government-backed guarantee, banks can approve loans with less collateral and risk.

- Networking: Involvement of SIDBI and DICCI connects you to industry groups and mentors.

- Non-collateral (up to ₹10L): Loans up to ₹10 lakh typically require no collateral.

- Women-centric: 80% of Stand-Up India loans have gone to women entrepreneurs. If you’re a woman founder, you may get priority.

When this scheme makes sense

- You belong to the target group. If you are SC, ST or a woman starting a new non-farm venture, it’s designed for you. (Men who are not SC/ST are not eligible unless they co-own a company with a SC/ST or woman majority.)

- You need substantial capital. Your project cost is high (over ₹10L) and you need up to ₹1Cr. If you only need a small loan (under ₹10L), other schemes like PM MUDRA Yojana may suffice.

- Your project is greenfield. It’s your first time doing this business. The scheme explicitly funds first-time ventures.

- You can arrange margin and equity. Have at least 10% of the project cost saved, plus be ready for up to 15% margin (though state/central subsidies can cover part of that).

- You want handholding. If you value the portal guidance and training support for making your business plan pitch-perfect, Stand-Up India is good for that.

Example: A tribal engineering graduate wants to launch a small solar-panel factory (greenfield). The project costs ₹50 lakh. This scheme lets her borrow that amount with little collateral and get mentoring for her business plan.

When this scheme may not be suitable

- Not in target group: If you are a general category man (non-SC/ST), this scheme is not for you. Also, if your business is not “new” (for example, you already run a similar shop or factory), you won’t qualify.

- Project size mismatches: If you only need a small loan (< ₹10 lakh), Stand-Up India might involve unnecessary formalities; consider other small loan schemes. Conversely, the project cost should justify the effort – it’s not ideal for tiny side hustles.

- Sector restrictions: Purely agricultural / crop loans are excluded. (However, allied activities like dairy, food processing are allowed.)

- Cannot meet contribution: If you can’t bring at least 10% of the money yourself, banks may not approve the loan.

- Risk of rejection: Government backing helps, but banks have full discretion. If your credit score is poor or business plan is weak, they can deny the loan. There’s no guaranteed approval just because the scheme exists.

- Overlapping schemes: If you already got support from similar schemes, check limits. For example, you cannot use Stand-Up India to expand an existing business (that’s not greenfield).

In short, Stand-Up India is best when you fit the criteria well and need a significant funding boost with institutional support. It makes less sense if your need is small or if you lack the required documentation and own contribution.

How the application process usually works

- Check eligibility and prepare documents: Confirm you fit the SC/ST/women + greenfield criteria. Gather KYC (ID, address), caste certificate, qualification certificates, business plan/project report, bank statements, and cost estimates (e.g. machinery quotes).

- Prepare a project report: A clear, simple project report (showing what you’ll produce, costs, revenues, loan needed) is crucial. This will be scrutinized by the bank. Many founders enlist local MSME consultants or DICCI mentors for help.

- Choose your bank branch: Not all branches are equally active in this scheme. It’s wise to approach a branch known for Stand-Up India or with a helpful LDM (Lead District Manager). Banks like SBI, Central Bank, or regional banks often have dedicated SME units. You can contact the local District Industries Centre for branch recommendations.

- Apply: You have three channels:

- Bank branch: Walk into the selected bank and ask for a Stand-Up India loan. Submit your form and documents.

- StandUpMitra portal: Register at standupmitra.in (powered by SIDBI). The portal guides you through steps and sends your application to banks/LDMs.

- Lead District Manager (LDM): The LDM office in your district helps applicants connect with banks.

- Loan appraisal: The bank will vet your business plan, credit history, and credit eligibility. They may ask questions or request clarifications. Stay responsive and improve your proposal if needed.

- Sanction and disbursement: If approved, the bank issues a sanction letter. You bring in your margin (10% own funds), sign the documents, and the loan is disbursed (often in stages tied to project milestones).

- Post-disbursement: Use the loan funds strictly for the business, as per the rules (banks track this). Begin repayment after any moratorium (max 18 months), up to 7 years total term.

Real-world tips: Prepare early by drafting your project report even before approaching banks. Attend a government skill/entrepreneurship workshop (DICCI, SIDBI events) to strengthen your plan. Check if your state offers additional margin/interest support. And always double-check that the branch manager knows about Stand-Up India; sometimes asking for the “SC/ST & Women Entrepreneur loan” by name helps.

Common mistakes founders make

- Thinking it’s free money: This is a loan. Some founders mistakenly believe the government will “cover” the loan – it won’t. You must repay with interest. Treat it as a standard bank loan and plan for repayments.

- Incomplete paperwork: A common error is to show up at the bank without a proper project report or lacking key documents (like a caste certificate). This delays or derails the application.

- Ignoring scheme rules: Some try to use funds for personal use or non-greenfield projects. Banks will reject or call back loans if rules are violated.

- Applying to any branch: Not all branch managers proactively know or like processing this scheme. It’s better to find a branch in your area that has already done Stand-Up India loans (the bank’s LDM can advise).

- Underestimating own contribution: If you plan on “10% own funds” but only bring 5%, the loan will be scaled down or denied.

- Paying middlemen: Beware of agents who promise quick loans. Banks do not require any fees for processing a Stand-Up India loan. A correct loan process has zero upfront charges (except your margin).

- Failing to follow up: After applying, don’t vanish. Follow up with the branch or portal portal, address queries promptly, and keep momentum.

Official source & verification

For credible information, founders should consult:

- Stand-Up India Portal (StandUpMitra):The official scheme portal (run by SIDBI) has FAQs, online application and status tracking.

- Press Information Bureau (PIB) FAQs: e.g. the Ministry of Finance press release (April 2023) answers common questions.

- SIDBI Website: Small Industries Development Bank of India (SIDBI) has scheme details and application guidance.

- DICCI Resources: The Dalit Indian Chamber of Commerce & Industry often holds scheme workshops and can guide applicants.

- Your Bank’s MSME Unit: Many banks have an official brochure or page on Stand-Up India (e.g., SBI, Bank of India websites have standalone pages).

- UMANG App: Indian government’s UMANG app lists schemes (though often one can only read, not apply).

Always verify any advice or third-party help against these official sources to avoid misinformation.

FAQs

Q: Do I get free money or a loan?

A: It is a loan, not a grant. You must repay it (over up to 7 years with ~18 months moratorium). No free handouts here – treat it as a subsidized bank loan.

Q: Can I apply if I already run a small business?

A: No. Stand-Up India is only for greenfield ventures – meaning your business must be brand-new in that sector. If you already operate a similar enterprise, you’re not eligible.

Q: Do men get this loan?

A: Only if they are from the SC or ST categories. General category men are not eligible. Women of any caste qualify as long as they meet other criteria.

Q: What if I only need ₹5 lakh?

A: For loans under ₹10 lakh, consider MUDRA Yojana or other micro-credit schemes first. Stand-Up India requires a formal process and is better for larger needs (₹10L+).

Q: Is collateral required?

A: For loans up to ₹10 lakh, banks typically waive collateral (thanks to government guarantee). For larger loans, partial collateral or third-party guarantee may be needed, but the scheme’s guarantee reduces your burden significantly.

Q: Can I get help preparing my application?

A: Yes. The StandUpMitra portal provides guidance and connects you to local mentors, training and even project report help. Also check local MSME/DICCI workshops for tips.

Q: Which banks participate?

A: All scheduled commercial banks can do this scheme. In practice, most large banks (SBI, PNB, BoI) and many private banks participate. The key is to find a branch where the manager has worked on Stand-Up India loans before.

Read More Blog-Building an AI-First Startup Culture

Eligibility Criteria

SC/ST and Women entrepreneurs (greenfield projects)

🚀 Ready to Scale Up?

Don't miss this opportunity! Visit the official portal to check your eligibility and apply today.

Apply Now on Official Website →

Comments are closed